Yahoo! and AOL Reshuffle

or, "At What Point Do You Stop Getting Called a Tech Company"

My first email account was, like so many other folks’, an @yahoo.com domain. Yahoo was, for a long period of time, the quintessential tech company. They were based in the Valley. They had cool offices. They effectively were the internet. Everyone had an opinion on them. They seemed idealistic, energetic, yet mysterious and confusing.

Sound familiar? Now replace Yahoo with AOL in that previous paragraph and tell me there is a difference? Or maybe try doing that same thing with Google.

Okay, so maybe the Google comparison is a bit hyperbolic. It’s not like there is any sign that Google is headed toward the same fate as those two early-aughts tech dinosaurs. But the point is, nobody would question that Google is a tech company. They are one of the tech companies of our age.

But when you think of AOL and Yahoo (now “AOL+Yahoo” in my head), you most likely don’t classify them as tech companies. For one, they are both privately held and don’t carry the same weight as some of the big tech co’s of the age. But, probably much more importantly, their parent company, Verizon, refers to them as Verizon Media. And now that they are being sold by Verizon for pennies on the dollar, the narrative seems to be more about Verizon’s media aspirations, and less about it’s tech goals.

(That Last One Is Pretty Brutal)

Again, Verizon Media is the technical name for these two assets, currently being operated under the Verizon corporate umbrella. This was the name that the execs at Verizon came up with after they tried to name the combined entities Oath, which, as is clear, didn’t really work out. For two and a half years, Oath toiled under the Verizon umbrella and didn’t achieve a great deal of success. The entity had a handful of missteps, including a fiasco with Tumblr that led to the ultimate demise of a once-promising social media platform (albeit, the “missteps” in question were likely extremely necessary and more a mark of bad deal due diligence, than company mismanagement). A further sign of the entity’s struggles were a headcount reduction of ~7% of the workforce in 2018. After two and a half years of floundering as the Oath corporate brand, Verizon renamed the entities to Verizon Media.

Calling former high-flying tech companies media companies might seem like an example of corporate negligence - big corporate folks not understanding their asset. However, this is actually a fairly accurate representation of the Oath/Verizon Media offering. Yahoo and AOL are media companies - a house of media brands, such as Yahoo Finance (which I still ride for), TechCrunch, Engadget, and Rivals, among others. They have some more tech-ish entities under these brands, but even those are particularly media-heavy, like Flurry, an analytics advertising firm.

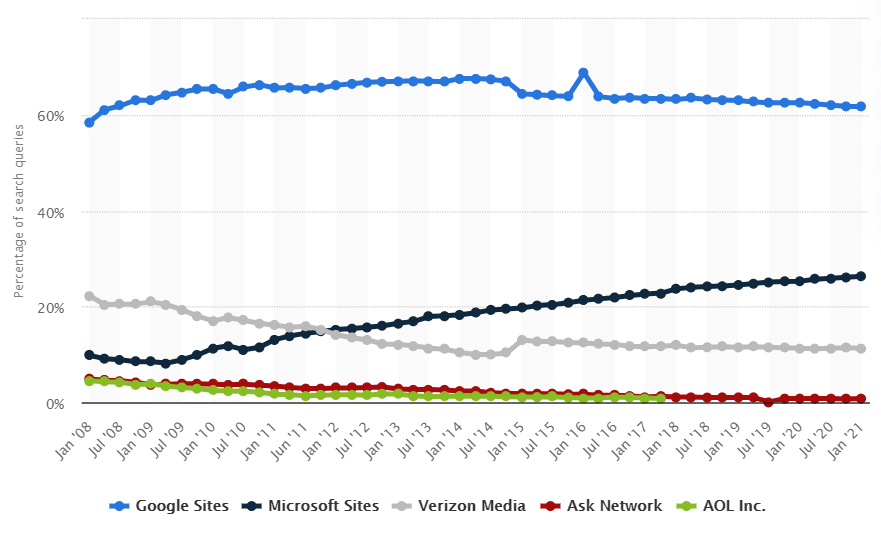

The entity’s main powerhouse was still it’s ad-platform. A true example of internet technology at scale. But this ad-platform had lost it’s groove. First, it’s search function had long since lost the search race to Google, and couldn’t even keep up with Bing (the chart below is gnarly). The ad-platform is also also comprised of display advertising technology, which was extremely in vogue in AOL & Yahoo!’s heydays, but has recently been beaten up by native advertising, ad-blocking technology, the rise of subscription media, and a variety of trends that have reduced the efficacy of digital ads (Facebook has eaten this space for breakfast, lunch, and dinner). Verizon Media also consists of ecommerce capabilities, which, if I am being completely honest, I didn’t even realize they had until the writing of this article.

While Verizon Media has some true “tech” attributes, it doesn’t have the core tech characteristic that drives valuations and narratives in that sector: high-flying growth. Since Verizon acquired AOL in 2015 and Yahoo in 2016, the two entities have, at best, stayed flat. In 2020, the division reportedly brought in $7 billion in sales. In the first three months of 2021, it had it’s strongest quarter in years, growing 10% from the same period prior year. While 10% is nothing to scoff at, it was likely built on the back of a bad March 2020, when advertisers reduced ad-spend in the midst of COVID-19’s initial outbreak.

To put that revenue number in perspective, however, when Verizon bought AOL in 2015, they had ~$2.5 billion in total revenue; when Verizon bought Yahoo in 2016, they had ~$5 billion in revenue. To even say that Verizon has held those two entities flat would be charitable.

Of course, it’s hard to say that this decline is clearly Verizon’s doing - both AOL and Yahoo were struggling prior to the acquisition and weren’t exactly growing like crazy under public ownership. Yahoo’s acquisition didn’t include the entire company, parts of it were split up, so it’s not a true apples-to-apples comparison. But no matter how you slice it, Verizon’s acquisition of AOL+Yahoo has been beleaguered at virtually ever step. The low point for this entity surely came in December 2018, when the aforementioned headcount reduction took place and Verizon took a $4.8 billion haircut on valuation on these two entities. At that point, the writing was on the wall. They started selling off important brands in 2019, and it seemed clear that Verizon was dismantling its media business. Yahoo+AOL would be relegated to the dustbin of history.

Then, a handful of days ago, it was announced that Verizon would be selling Verizon Media to Apollo Global Management at a reported $5 billion valuation.

This deal isn’t inked just yet, but if you think about the one multiple we can back into (Revenue), this doesn’t look all that expensive at 0.7x when compared to any tech companies and a lot of media companies. Valuing a company of this size using a revenue multiple is a bit of a futile gesture, especially when that revenue is not growing, but it’s the one benchmark we have.

To better understand Verizon Media’s results, you can dig into Verizon’s 10K from 2020, where they do have several comments about how the COVID-19 pandemic interrupted parts of their Media business as advertisers reduced their overall ad-spend. There are also some articles that came out at the beginning of the year commenting about how the division was starting to see some real success since AOL and Yahoo! acquisitions were both completed.

But it’s tough to understand the trajectory of Verizon Media / AOL+Yahoo. Apollo is one of the most successful PE Groups in existence, and seemingly grow their assets exponentially, on the backs of wild operational success. If they are making this purchase, then surely they see something positive, right?

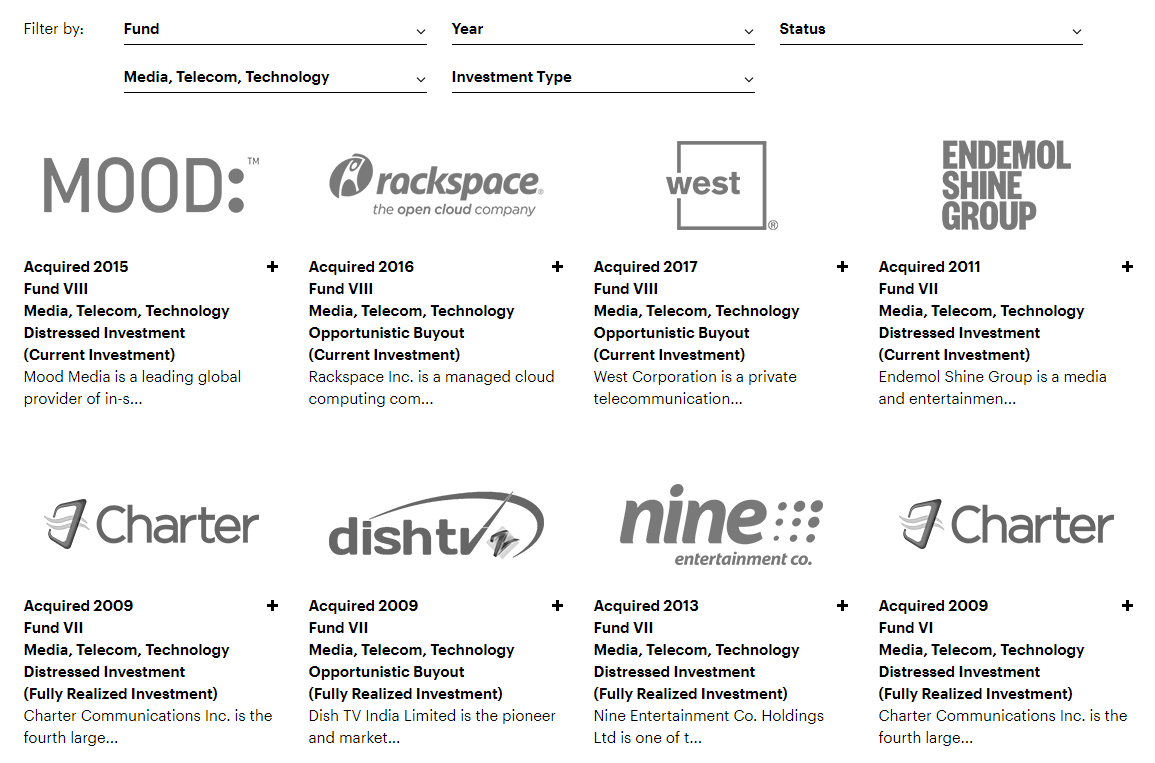

But when you look at Apollo’s assets that fall under the category of “Media / Telecom / Technology”, it doesn’t exactly inspire confidence in their ability to manage a media/tech asset like Verizon Media. In fact, it makes them look more like Telecom vertical that dabbles in tech and media, and less like a full-fledged TMT group.

But what is it that Apollo sees in AOL+Yahoo? It could be that it is an asset that still has a decent amount of users and generates a fair amount of revenue, but has completely been mishandled by its corporate overlords. Or maybe the price was just too attractive to pass up. Or maybe Apollo just wants to take on more aggressive risk in the current economic environment.

Who knows exactly what their motivations are?

In an internal memo circulated to Verizon employees, Verizon CEO Hans Vestberg said the following:

“After a strategic review, Guru and I discussed, and believed, that the full value of Media’s offerings have yet to be unlocked. Apollo has a powerful vision that includes aggressively pursuing growth areas in commerce, content and betting. One that also features synergies with many of the traditional brick-and-mortar companies in their portfolio who can benefit from Media’s e-commerce platform. What made Apollo’s offer so appealing, is that it includes leveraging the entire Verizon Media ecosystem of adtech, affiliate relationships, data, insights, targeting and reach.”

So while Verizon Media continues to struggle, the party line is optimistic that Apollo can make lemonade out of lemons. Of course, they wouldn’t say so otherwise and Apollo wouldn’t do this deal if they didn’t think they could turn things around.

Based on AOL+Yahoo’s current market positioning, I think there are a handful of paths the entity could go do to drive future growth and get back on top:

Gaming: The past several years have seen a historic rise in the popularity as well as accessibility of online gambling. There are a ton of companies that have become glamour stocks (see: Penn Gaming) on the back of this sports gambling narrative, and it’s possible that Yahoo could ride this wave even further. The entity already has an installed based of gambling users and has access to several gambling jurisdictions worldwide. They already act as a marketing partner for a handful of gambling platforms, such as BetMGM. They are an established player that needs some further investment to start capturing market-share. Entering a gambling market is not a cheap endeavor, however, and this would require pretty significant investment from the Apollo folks to make work.

Ecommerce: As I mentioned earlier, I didn’t even realize that AOL+Yahoo had an ecommerce function housed in Verizon Media. As a result, I find it hard to believe that they are exactly tearing up that market currently. Much like the gambling sector, ecommerce continues to rise at a rapid rate. If Apollo can help AOL+Yahoo ride that wave more effectively, they could potentially unlock some serious value. And while a lot of folks considered the ecommerce battle to be over and won by Amazon, Shopify has shown that there is room to succeed in the ecommerce industry, despite the Everything Store’s reach and power.

900 Million Users: I have nothing clever for this, but Apollo could do something, literally anything, with its 900 million users. That is about the same as Twitter, Snap, and Reddit, combined!

I definitely believe that potential exists here for Apollo. They are getting a huge user base at what might be considered an attractive multiple and have some clear growth opportunities to focus on. But Apollo won’t be AOL+Yahoo’s first corporate overlord to feel the same way about the entity. But clearly Verizon wasn’t the company to unlock that value. Verizon likely needs to focus on a myriad of other things instead of getting sidetracked in the ultracompetitive world of tech and media. If more-of-the-same takes place under the guidance of Apollo, it’s very possible that we will no longer be reading about AOL+Yahoo in the Wall Street Journal, and instead only see their names in history books.