Social Media Inflection Points

Elon, Twitter, Snap, TikTok, And Everything Else

Disclaimer: Newsletter and the information contained herein is not intended to be a source of advice or credit analysis with respect to the material presented, and the information and/or documents contained in this website do not constitute investment advice. Opinions contained within this letter are my own and not those of my employer.

Elon Musk recently bid (and won said bid) on ownership of Twitter.com, the incessant social media platform that I love dearly. As with everything the Technoking of Tesla does, this has caused some… controversy. Critics are claiming that Musk’s Twitter will amplify right-wing voices, destroy democracy as we know it, or maybe just createerrible product experience. Elon fans are proclaiming this as the turning point for the bird app - he’s the greatest entrepreneur of his generation, he’s got the technological Midas touch, he’s real life Tony Stark - you’ve heard this version of the story before.

Of course, with any transaction, it’s important to review the actual deal details, as price is only a small piece of the equation:

$43.4 billion purchase price, $54.20 per share

Funds for deal: Morgan Stanley + other banks providing $13 billion in financing, $12.5 billion of margin loans (via Musk’s equity portfolio), and Musk writing a $21 billion equity check.

The Company currently has $5.07 billion in TTM Revenue, which represents a 8.5x Revenue multiple

Adj. EBITDA of $950 million represents a 45x EBITDA multiple and a leverage ratio of ~13x. Which is a lot of leverage.

Assuming a 6.5% Interest rate on the bank loan, the Fixed Charge Coverage Ratio is pretty thin, depending on how it’s calculated.

$1 billion termination fee for acquisition entity (Musk)

Proposed Closing Date: October 24, 2022

Legal opinion on the merger agreement via NY Times: “It’s actually a pretty plain vanilla merger agreement,” said Steven Davidoff Solomon, a professor at the School of Law at the University of California, Berkeley.

If this were a deal put together by a typical buyout shop or some other investment vehicle, it might make you scratch your head. That’s a lot of leverage and those multiples, considering the current state of the tech market, are pretty rich. Sure, it’s not a super crazy premium on what the business was trading at pre-deal, but it’s not like the stock was moving in the right direction.

But, of course, Elon isn’t acting like a typical investment fund or buyout shop. The thing that makes him such lightning rod is that he doesn’t do anything typical, or at least he tries hard to make it look like he’s atypical. He’s not the first activist investor to take a company private for improved gains like this. Based on a recent series of tweets, he has made it very clear that he is going to make some changes to Twitter. His ownership is not contingent purely on macro-headwinds - he has a turnaround plan (or at least a general sketch of a plan).

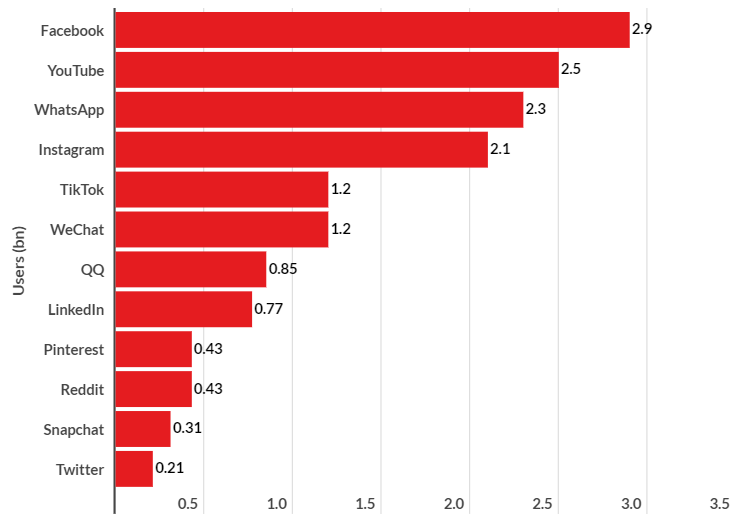

And, to be clear, Twitter is a beleaguered company, so it’s not insane to think a turnaround is needed. They are on the low end of users when compared to other global social media sites, lagging behind Snapchat and even Pinterest, and languishing for better growth for years. It is a lightening rod for political infighting, frequently becoming the center of the free-speech debate, despite being at the bottom of the barrel as far as social media sites are concerned. And while topline revenue growth has picked up in the past several years, it’s nothing compared to some of its tech-giant peers, who are growing larger numbers at a faster clip. The Company has displayed an ability to have positive cash flow at times, but nothing on a grand or impressive scale. It has limited growth compared to expectations, does a poor job of capturing capital returns, and still somehow seems to be the platform that gets dragged in front of congress the most.

It would be really easy to lay this all at the feet of Twitter and its management team. And maybe Musk is exactly the right person to come in and shake up the much besieged social platform - he has shown a proclivity for garnering turnaround success in big companies. If Twitter’s problems are purely financial, he might not be the right guy for the job as his skill set doesn’t seem to lie squarely in the “financial controls” leadership category. But if it’s growth or outside-the-box thinking you are looking for, he might be up to the task.

It’s not just the internal company picture worth considering, but also the macro social media landscape to take into account. Musk might be buying the business at an important inflection point, when social media status quo likely wont stick around for much longer.

First, let’s look at Meta, which announced at the start of the year that user growth had hit a ceiling for the big blue app, losing daily active users for the first time since being a public company (and probably ever). The Company has not recovered since, having given up a third of it’s value.

YouTube, which has been a stalwart in the social landscape for quite some time, has also shown signs of slowing down, with ad revenue missing analyst expectations for the first time in its reporting history in Q1 2022. Many are blaming YouTube’s decline on TikTok’s rise and the rising inflationary environment, which has historically hit the advertising business hard.

There is Snapchat, the disappearing messaging app, which seems to have righted it’s ship since noted user declines in 2018, and has posted +20% user growth year-over-year for each quarter since 2020. Although that rate of growth does seem to be slowing down a tiny bit, with only 18% growth in Q1 2022. The Company was effectively left for dead during it’s darkest hours in 2018, but seems to have reverted the narrative and is one of the bright spots in the social media landscape.

There is a social media platform that many will/have pointed to in regards to eating market share of a lot of these platforms: TikTok. The Chinese social giant has exploded with growth, particularly accelerated during the pandemic, and capturing more and more market share, while other platforms seem to be slowing down. And maybe the explanation for other social giants losing steam is the simplest one: social media attention is a relatively zero-sum game, where there can be only one true winner, and for the next several years, that winner is going to be TikTok.

But if you dig in a little more, you can find that even TikTok has shown some (albeit, relatively minor) signs of slowing down. ByteDance, TikTok’s corporate parent entity growth rate slowed down in 2021, well below expectations. And while this certainly isn’t enough to say that the end is nigh for TikTok, it does highlight that the platform has it’s own problems, especially in the US. It is also a political lightning rod, having drawn scrutiny from both sides of the political aisle and even drawing questions about whether or not it is a national security threat. While it may stay on top for a long time considering its current growth curve, it has enough bogeys out there threatening its position.

The Social Media landscape is at an inflection point: former winners are going sideways, signs of cracks in armor are exhibiting themselves in stalwarts, and foreign entities are displaying an impressive ability to capture market share while simultaneously facing their own problems. There are way more question marks today surrounding the state of social media than there were three years ago, and things seem to just be getting stranger.

There are a lot of questions as to why these companies are hitting a wall. Recently I heard an excellent explanation of what’s going in this space from Nikita Bier when discussing similar issues at Netflix. He referred to the problem as product decay - which is what happens when growth hacking goes too far. The example he provided was ranking content in a baity way - in other words, pushing stuff out that would improve Netflix’s numbers at the expense of a user’s actual experience, thus reducing the overall value of product to said customer. He even gave a similar example for Facebook, which was the king of growth hacking for a while, but seems to have run out of hacks and is the ultimate case study of when growth goes wrong.

And growth hacky stuff has worked for a while as the story surrounding consumer social relied heavily upon just new people coming online every day. But as the internet has become ubiquitous and COVID finally forcing everyone onto social platforms, the equation for growth has changed. Now it’s becoming reliant on good technology and improved experience, not just hacks. Netflix, who no longer can rely on simply expanding into new markets and pumping money into the content development game, now has to create content that is high quality if it wants to win its market. The same is true to products in the social media sector.

I am being a little reductive when ascribing social media’s problem to just one cause. Ultimately, there are probably a plethora of reasons why growth has slowed in the consumer social space. But that doesn’t mean it has to stay that way, or that consumer social is over. It just further validates that we are likely at an inflection point in the industry, and that Musk’s purchase of Twitter might actually be a watershed moment in the industry.

It is possible that Elon is buying Twitter at exactly the right time, able to upend the market with changes to product, strategy, etc. It’s also possible that he is loading it up with debt he and the Company can’t really afford to pay off and will wipe Twitter off the map altogether. He clearly has an impressive track record and knows a thing or two about technology companies.

Whatever happens to social over the next 12-18 months is going to be interesting to watch. This stuff clearly impacts the world we live in. We are well past the point of thinking these platforms are just toys, or only kids are using them. Social media is as important to our economic engine as the auto industry, if not more. So keep your eyes peeled and, no matter what, keep tweeting through it.