S-1 Review: Justworks

Disclaimer: Newsletter and the information contained herein is not intended to be a source of advice or credit analysis with respect to the material presented, and the information and/or documents contained in this website do not constitute investment advice. Opinions contained within this letter are my own and not those of my employer.

Company Overview

Justworks is a human capital management (HMC) company that services SMBs (small and medium sized businesses) by providing benefits, payroll, human resources and compliance support through its proprietary cloud-based software platform. The Company was founded in 2012, having raised nearly $143 million of venture capital since then. The most recent round (Series E) was raised in January 2020 at an undisclosed pre-money valuation (although I would expect it’s somewhere south of $1 billion). The round was led by Union Square Ventures. Other investors over the years have included FirstMark, Redpoint, Thrive, and Bain, among others.

The Company is led by founder and CEO Isaac Oates, who has an impressive background, including engineering and product stints at Amazon and Yahoo in the Aughts, Etsy as a special projects manager, and time in the US Army Reserve. He also got his undergrad degree from the much lauded University of Illinois’ computer science program. While he is probably the highest profile member of the executive team, they do have some seasoned veterans onboard as well.

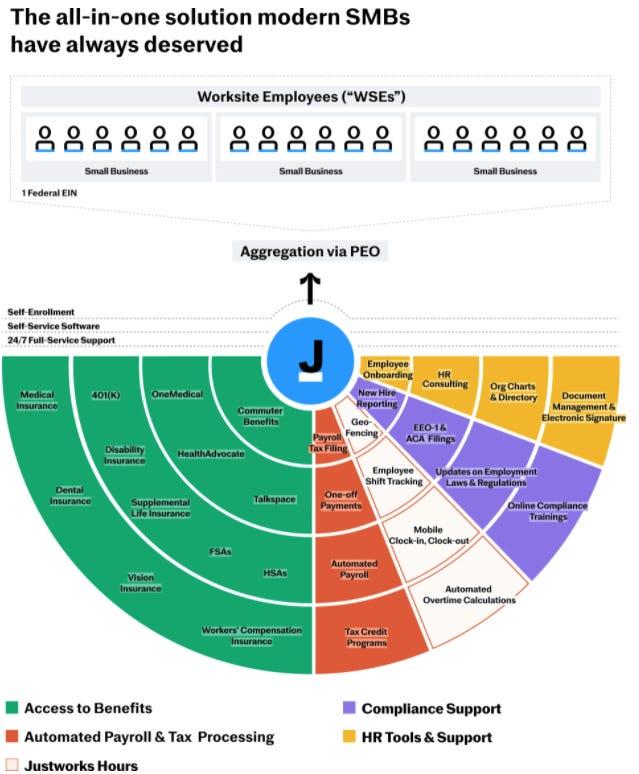

Focusing more on what the Company actually does, in more traditional HR parlance, Justworks is a PEO (Professional Employer Organization) - an organization that enters into a joint-employment relationship with an employer by leasing employees to the employer, thereby allowing the PEO to share and manage many employee-related responsibilities and liabilities. For you real-estate heads out there, think of a PEO as the sale-leaseback equivalent for HR services. This allows employers to outsource various HR functions, like employee benefits, compensation and payroll admin, workers comp, taxes, etc. PEO’s are the employer of their clients’ employees - this provides economies of scale by having more benefits options for its employees as well as reduce the HR administrative burden that most small businesses can’t afford to manage themselves.

To better understand the structure, see below, from the S-1:

It should be noted that PEO’s have been around for a long time and several companies have grown into multi-billion dollar enterprises off the back of a PEO’s solid customer value proposition and business model. Justworks is the most recent in a long-line of fast-growing HCM software platforms that are actually PEO’s when you look under the hood. The Company is attempting to refresh the PEO business model by wrapping it in slick software and acquiring customers like a tech company. Although that is not necessarily a good thing (I don’t know if you have heard, but customer acquisition costs have gone up a lot recently), it can be an effective way to break into a market and gain market share quickly.

To assess this growth, one of the Company’s KPIs is Worksite Employees (WSE), which just means an employee that one of their customers have on Justworks’ platform. At the time of the Company’s Series E fundraise in 2020, it had 86,000 employees on its platform. At the time of the S-1, the Company has more than 140,000 employees on the platform. It has certainly put that $143 million of raised venture capital to work, growing it’s base significantly and grabbing market share quickly.

Further breakdown of WSE’s by year:

2014: 300

2015: 1,900

2016: 8,000

2017: 17,000

2018: 37,000

2019: 69,000

2020: 89,000

2021: 118,000

Today: ~140,000

There are a lot of ways that a company like Justworks can grow its user base and revenue quickly - investing a lot in sales and marketing, building an incredible product, solving a previously unaddressed problem, just to name a few. It’s hard for a finance guy like me to really effectively assess how much product has led growth, but I found the following quote from the Series E fundraising announcement to be enlightening:

“Justworks has raised the bar on what people can expect from a PEO,” said Fred Wilson, partner at Union Square Ventures. “Their software is elegant, intuitive and easy-to-use, and Justworks’ technology and operating model allows them to serve small and medium-sized businesses better than anyone else in the market. This has led to rapid growth and, more importantly, the creation of a category-defining offering that drives levels of customer retention and satisfaction that are simply unheard of in the HR services space.” - Fred Wilson

What’s more, the PEO model is certainly one that has merit in the marketplace. In the S-1, the Company calls out several pain points that it alleviates for its customers:

Human Capital / People tasks require an outsized amount of time for managers

SMBs struggle to retain talent due to the relative cost of securing benefits packages in-line with what larger organizations are able to offer.

SMBs have a higher regulatory burden, “particularly those with geographically distributed teams”

So while they may not have a necessarily revolutionary product (there are a lot of PEO’s and HCM software platforms out there), they are solving a real problem. And if they do it better than their competitors, that can go a long way.

The Company also points to a couple of things to show its products and services are satisfying their customers, including a five-year average 58% Net Promoter Score (well above HR industry average) and a 117% subscription net revenue retention rate in the last fiscal year. The Company also maintains that it has been historically able to hold onto customers who outgrow their traditional target customer employee size, however does not provide any significant detail to back that up. It’s hard to say for certain how strong the product is compared to its competitors, but it’s at least doing something right.

Beyond product excellence - which is admittedly hard to quantify - a core part of the Company’s strategy is its go-to-market efforts. This includes an inside sales team for established SMBs and an automated self-enrollment funnel for emerging businesses. The self-enrollment channel represents ~15% of new business in the most recent LTM period. The LTV:CAC ratio (an efficiency measurement of a customer’s value and how much it costs to acquire said customer) for the business is 5.7x, which is very strong for a business at this stage. However, there is potential that it is too high and the Company is missing out on potential market share by not spending enough money to acquire its customers. An academic view of LTV:CAC would say that 3.0x is the sweet spot for the ratio - spending the right amount while also being appropriately aggressive in capture share of the market. However, it doesn’t always shake out that way in the real world. This could also be a sign that the product “sells itself” - again, that’s very hard to verify.

Ultimately, the Company is hanging it’s hat on it ability to grow and to grow at scale. While 32% growth year-over-year is not exactly setting the world on fire for a company that has raised $143 million of venture capital, it’s nothing to look down upon either. In order to maintain momentum, the Company is going to continue to pursue various growth strategies.

One of those growth strategies is increasing monetization with existing customers. The companies that Justworks currently services are traditionally well below the 100 employee threshold (average size of 18 WSE’s). However, as those companies grow, Justworks wants to continue to grow alongside them. That makes sense for companies that have traditional growth profiles, but for any of its customers who are high-fliers (read: startups raising significant capital), it seems as though they will eventually outgrow the PEO model. It should be noted that the Company provides various case studies of customers in its S-1, and almost all of them are tech startups in some form or fashion. It is somewhat of a meme for a startup to only sell to startups and that growth is more funded by the venture ecosystem than would appear at first blush. The Company does have handsome net revenue retention rates (above 100% in the past two years), which is evidence that growing with their customers is not total hogwash.

The Company does have some geographical concentration currently, with nearly 53% of its customer base being located in the greater New York City area.

Industry Overview

The Human Capital Management Software market is approximately $18 billion and is expected to grow at a healthy clip over the next several years. The market consists of point solutions, fully outsourced HR services, and everything in between. The Company deploys a PEO product into the marketplace because it believes that is the best way to assist entrepreneurs and managers of SMBs - almost completely removing the administrative burden of the majority of HR tasks.

The Company is explicitly targeting SMBs, instead of going after big whales, as it believes this is an underpenetrated part of the market. While large corporates probably pay better and are more attractive, Justworks believes that it has a better angle for customer acquisition of SMBs than the rest of the market. Much like some of the insurtech names of the past couple of years (Root, Lemonade, etc), Justworks thinks it has developed a better mousetrap and can acquire SMBs more effectively and efficiently than existing incumbents, thus gobbling up market-share while still maintaining healthy margins. Of course, things haven’t worked out so great for those insurtech carriers so far; LMND’s chart is not for the faint of heart.

It should be noted that this theory is not without validation. There are a lot of SMBs out there in the United States. According to the Company, there are 40 million people who work for companies with less than 100 employees currently. According to the SBA, there are approximately 6 million SMBs that employ more than one individual. The Company currently has 8,000 customers that it services, which represents only ~0.1% of market share - either signifying room for growth or difficulty capturing market share.

The Company calculates it has an approximate addressable market size of ~$40 billion. This is based on an estimated 29 million addressable employees in its core target market and an annualized contribution profit per employee per month of $113 for the most recent TTM period.

The Company lists several trends which are beneficial for its future growth prospects:

Millennial and Gen Z populations prefer a self-service model with limited touch points. The future of the workforce (more than half of all employees by 2026) prefer to have their various HR issues resolved by an outside party than by the company they currently work for.

Businesses are using more digital work processes. I don’t know if you have heard, but software is eating the world.

Businesses are increasingly geographically distributed. The rise of remote work makes the administrative burden of human capital management even more significant as each geography and region an employee works in requires a separate and unique set of rules and regulations. City and state insurance requirements are hard enough to deal with when everyone is located in the same place. Now imagine having an employee base of 50, with 27 different states represented - there is no way one HR professional can handle that entire situation.

Regulation of employee benefits are becoming increasingly complex and expansive, making PEO’s more attractive. Regulators gonna regulate.

Talent Acquisition and retention are becoming increasingly more competitive. It’s tough out there looking for solid talent. Having good benefits can help give you an edge. At the very least, good benefits are table stakes at this point.

While there are plenty of tailwinds for the industry, it’s hard to know if the Company is addressing them as effectively as its competitors.

Competitive Overview

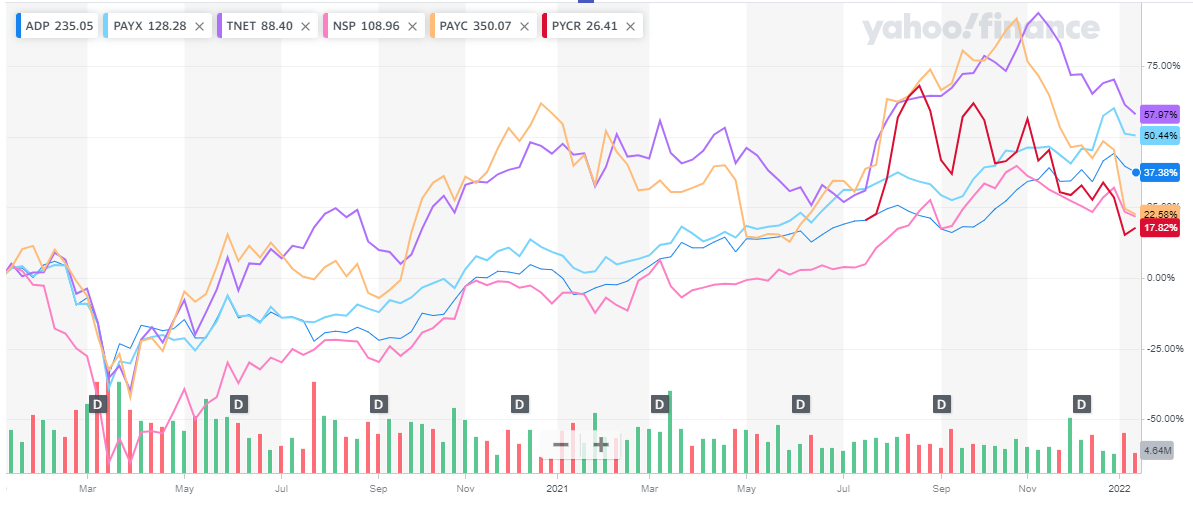

From the S-1: Our competitors vary across different markets and range from highly-specialized point solution software packages to a full-suite of integrated HCM solutions from legacy PEO providers and payroll processors such as ADP, Paychex, TriNet, and Insperity, SMB-focused payroll processors such as Intuit and Gusto, cloud-based HCM and payroll software providers such as Paycom, Paylocity, and Paycor, smaller regional PEOs and payroll processors, and other in-house solutions that offer limited functionality and/or scalability.

The industry is filled with competitive pressure, with several behemoths, as well as as some plucky upstarts, and folks in the middle. The Human Capital Management space is certainly not a blue ocean opportunity, but there are a lot of folks chasing after it because it has an attractive financial profile.

Quick profiles of the companies listed as competitors:

ADP: the 800 pound gorilla in the room, ADP has a $99 billion market cap. The company employs 56,000 employees. It operates in the cloud-based human capital management solutions space, specifically in PEOs and Employer Services. It is currently trading at an EV/EBITDA multiple of 24.9x

Paychex: About half the size of ADP, the company has a market cap of $44 billion and employs 15,000 employees. The company offers an incredible robust suite of services, mostly in the human capital management space, but it also provides insurance coverage. It is currently trading at an EV/EBITDA multiple of 24.4x

TriNet: The company is on the smaller end of more traditional HCM solutions providers, with 2,700 employees and has a market cap of $5.8 billion. The company is younger than ADP or Paychex and is based on the West Coast. They also have a full suite of HCM services. The company currently trades at an EV/EBITDA multiple of 12.6x.

Insperity: The company is a similar size to TriNet, with a market cap of $4.3 billion and 3,600 employees. The company currently trades at an EV/EBITDA multiple of 20.8x.

Gusto: The company is actually currently private so not much information is known at this time. However, it has raised nearly $691 million in venture capital funding and most recently raised a Series E financing round at a $9.5 billion valuation. Gusto’s customer base, at the time of its most recent financing, was around 200,000 (assuming that is ~equivalent to WSEs). It should be noted that Gusto is not a PEO. The company is anticipated to go public in 2022.

Paycom: The company employs 4,200 employees and has a market cap of $25 billion. The company’s current EV/EBITDA multiple is 87.6x.

Financial Overview

The Company drives revenue by selling subscriptions to its HCM SaaS product, as well as providing benefits to its PEO customers. For its SaaS product, it charges its customers on a per employee per month basis. Revenue is also derived from insurance-related billings and administrative fees for operating the PEOs. Although it may not be as sticky as SaaS revenue, the fees charged to PEO customers are somewhat recurring in nature - it’s pretty hard to switch benefits providers over night.

The Company’s total revenues for FYE May 31, 2021 were $982 million, a 32.4% increase over the prior year’s $742 million in revenue. The revenue mix is split between two categories: subscription revenue, which makes up $87 million in revenue and benefits and insurance related revenue, which makes up $895 million in revenue in 2021. During 2021 and 2020, the gross profit for the Company was $106 million (10.8%) and $77 million (10.3%), respectively.

From an operating profit perspective, the Company was able to actually turn a profit, albeit, a minor one. This was largely driven by reducing sales & marketing expenses in 2021 by nearly $12 million, despite significantly growing its base of customers and revenue. This decline was due to reducing advertising spend, lower compensation costs and decreased travel and entertainment expenses. The Company does expect to increase sales and marketing spend in the near future, but it obviously does not clarify how it will do so. It can be expected that at least part of the sales and marketing (and thus, the overall operating expense margin decline) is due to COVID situations. It should be expected that, at the very least, compensation expenses in the sales and marketing department are going to continue to climb in line with the ongoing labor wage inflation felt in most industries. There is evidence of this happening in the most recent reported quarter for the Company.

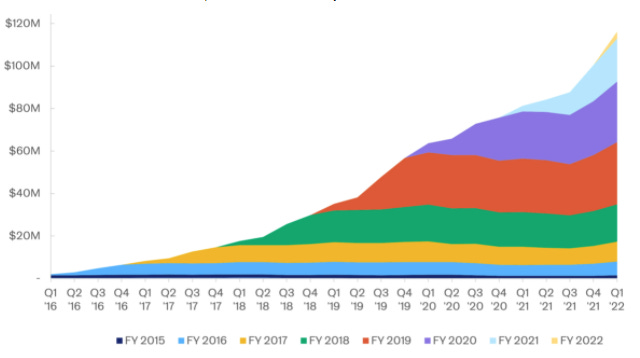

From a pure SaaS perspective, the Company does calculate a current ARR of ~$120 million. The chart below depicts the Company’s subscription revenue ARR by annual customer cohort.

The Company actually was cash flow positive in 2021.

Summary

While I was working on this publication, the Company announced that it would be delaying it’s planned IPO, without a date given for expected market restart. This likely speaks more to existing market conditions (especially for growth/tech stocks) than it does about the Company. The Company’s targeted valuation range is $2 billion. While we don’t have an adequate adjusted EBITDA number to compare this to on a multiples basis, from a revenue perspective, this is roughly 2.0x. Paycor, who recently went public in this space is trading at a 15.1x EV/Revenue multiple. Paycom, ADP, and Paychex all trade well above that 2.0x mark as well.

I am not a sellside analyst, so I don’t give buy/sell ratings on any stock that’s about to be traded on the public markets, but I do think this is a good case study to follow. This is a high profile example of the tech-enabled services business / wrap-it-in-software solution that is very popular in startup land these days. This is likely to act as a proxy for the startup / tech scene over the next couple of years as it continues to bring in startup customers and rides their growth.