Industry Graveyards

And the Night of the Walking Dead

There have been a lot of pronouncements recently about the upcoming bear market (or just a general, run-of-the-mill economic recession). The uncertainty caused by a cadre of factors (ongoing COVID lockdowns, war in Europe, inflation, bees dying at an alarming rate, movies all being sequels, etc.) has made the public and private markets skittish. While the carnage experienced in the public markets hasn’t quite trickled down into early-stage venture land just yet, it could happen any day. It could also not happen - seed stage venture is an extremely laggard sector of the investing industry, and while it does do some mirroring of the broader market, it certainly isn’t a 1:1 translation.

This is important to keep in mind when thinking through the potential for carnage at the startup tech landscape. Private markets have longer time horizons. They are also much less liquid. And while they will certainly experience pain if the broader market experiences it as well, it won’t necessarily share the same attributes and features of a public photo-sharing company halving in value over the course of a day (read: Snap, Inc.) or a enterprise software company guiding it’s growth expectations to 100% YoY and getting hammered in the after market trading (see: Snowflake).

A well-known, still important to remember truth: companies are very hard to start, no matter the environment. Hyperscale tech companies are extremely difficult. It takes incredible precision, strategy, execution, and luck to pull it off successfully. There’s a reason so many people counsel budding entrepreneurs on all of the risks they will face. There is a lot of advice out there, because there are a lot of corners one needs to look around. But critically, even the best founders, with the best support, and all of the capital in the world, will still fail sometimes.

Failure abounds in the technology world. But in most circles, failure is pseudo-celebrated because risk is appreciated. The risk of starting a business is no small thing. And so folks who have seen it before and spend their time around tech companies recognize that a lot of them end up in a graveyard. There are those that would lead you to believe that the tech bull run has been going on for the past 15+ years, and that it’s been all sunshine and rainbows, without any risk or failures. These were halcyon days, if some were to be believed. But that’s obviously far from the truth. Has it been easier than other periods of time? Absolutely. But that doesn’t mean there aren’t plenty of graves filled with aspiring companies that just didn’t cut it.

So the boom and bust cycle of startup land is not as black and white as it might appear if all you follow is the NASDAQ or FAANG (or any other tech acronym). There have been entire sectors of tech investing that have risen, fallen, and come back from the dead several times over since the last tech winter. When someone says “tech”, it’s important to understand what they mean. Is it just enterprise software? Or crypto? Or anything based in the valley and funded by a Midas-list venture investor?

No, the truth is the tech is an extremely broad term. And there are little booms and busts that happen every year.

A couple of examples of recent tech graveyards:

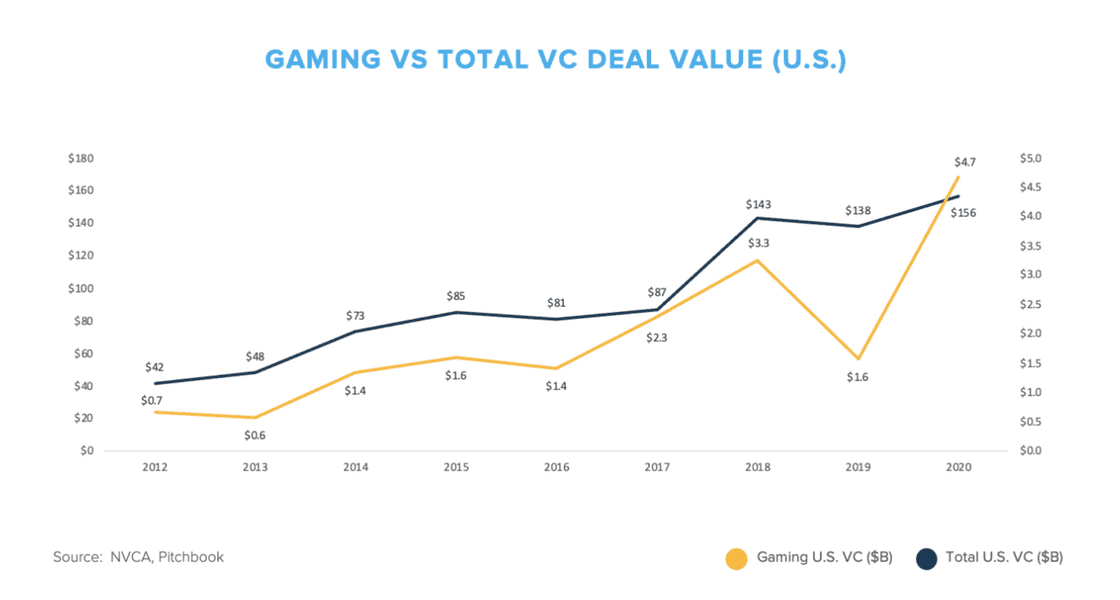

esports - competitive video games were the trend of the moment in 2017 and 2018. In 2018, $3.3 billion was invested into the space by venture investors, up from just $600 million in 2013. Then, in 2019, things fell off of a cliff. And for a while, it appeared that maybe esports just wasn’t a venture-viable business segment.

Artificial Intelligence - funding for artificial intelligence startups started to ramp up during the last decade, and hit new highs in 2020 when the venture market funded $61 billion of new investment into ai startups. In 2021 that figure grew by 87% to reach $115 billion. And while there hasn’t been any real sign of slowdown (except for the fact that this 87% growth rate in funding was actually below the software venture funding overall growth rate of 2021), it hasn’t stopped AI from becoming a punch line. It is now a running joke that every company who puts AI into their startup pitch deck is really just running fancy regression analysis (I didn’t say it was a good joke).

Blockchain - not really sure I need to spend too much time on this one, other than to say that Long Island Iced Tea renamed itself to Long Blockchain in 2017, causing it’s stock price to rip briefly. It is now delisted.

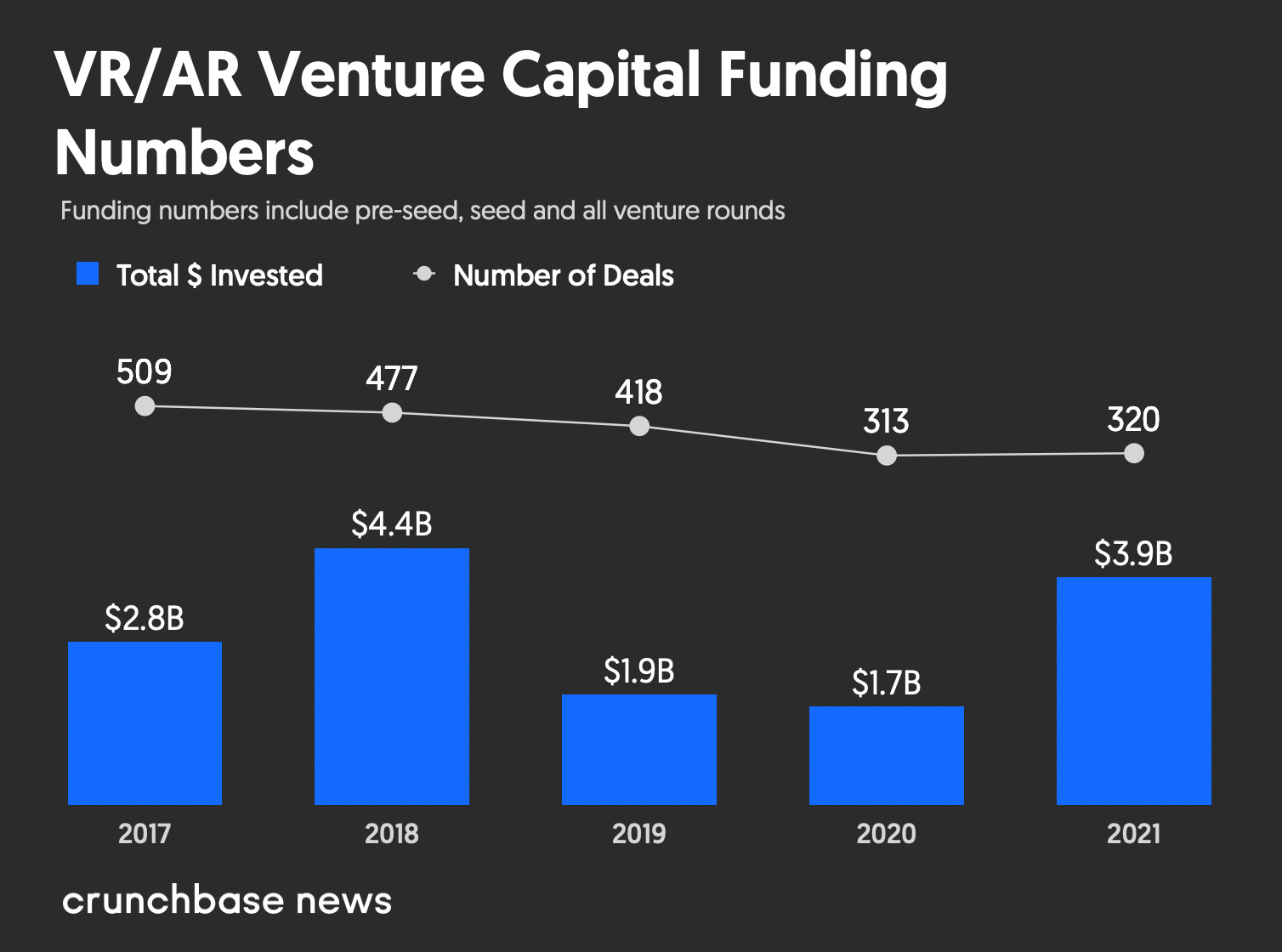

AR/VR - Virtual reality has been heralded as the new, new thing for a quite some time. When Facebook acquired Oculus in 2014 for $2 billion, it was viewed as a turning point for the industry. It was only a matter of time before Ready Player One became a reality and everyone would spend all of their time locked into a virtual reality. Recently, that seemed to be further on track, when Facebook renamed to meta and declared full-scale intent on trying to bring the metaverse fully into the world. But again, if you dig into the numbers in 2019 and 2020, that doesn’t fully paint the picture of an unbridled bull market.

The point is not that these are no longer interesting trends. Far from it: some of them are more interesting than ever. But they were at one point the hottest thing anyone had ever talked about. Depending on the year, it was impossible to read through a pitch deck without seeing a mention of one of these trends. Now, they don’t necessarily get all of the respect they deserve. From the graveyards described above, there are plenty examples that the dead are starting to walk, and walk among us.

esports has seen a significant jump in viewership since the pandemic, and, notably, a16z just launched a Games Fund I, a $600mm fund dedicated to the gaming industry.

AI - any VC knows how much more sophisticated the machine learning market has gotten over the years. But notably, breakthroughs in the AI space seem to be collecting at a remarkable pace. For instance, dall-e.

Blockchain - while I don’t have nearly as positive of a spin for the blockchain world, it’s worth noting that a pretty significant amount of volume is occurring on crypto protocols, like Ethereum, which averages 1 million transactions per day.

VR - In 2021, Oculus alone sold more headsets than Xbox sold consoles. It still has a ways to go before it catches up to PlayStation and Nintendo, but it’s a sign that wider adoption is starting to take place.

There are still great companies being built in all of these spaces. They have outlasted the hype cycle that accompanies a lot of new startup trends. At times it was easy to raise capital if you had VR in your pitch deck - other times it probably felt impossible. You probably had a harder time trying to get customer meetings set up or hiring good talent at a reasonable price.

I am not saying that the upcoming / impending / much-prognosticated-about recession is going to be similar to what a startup experiences on an industry-to-industry level described above. I also am not going to do any prognosticating myself about what a startup or startup investor should do during times like these - I was 8 years old during the dotcom bust, what the hell do I know? But tech industries go boom and bust all the time, more than just one market cycle.

Starting a startup is hard. There are definitely times to do it that are easier than others. But it can be done at any time - you just need to calibrate your strategy appropriately and work with the best possible partners you can find.