Columbus Netscape

Root's IPO and the Future of Ohio Tech

Newsletter and the information contained herein is not intended to be a source of advice or credit analysis with respect to the material presented, and the information and/or documents contained in this website do not constitute investment advice. Opinions contained within this letter are my own and not those of my employer.

In case you were wholly unaware, auto insurance is a massive market. Some estimates have it pegged somewhere in the $250 - $350 billion range. While that likely doesn’t crack the top ten largest industries in the US list, I wouldn’t be surprised if it’s somewhere in the top twenty five. It is a highly regulated financial product that is nearly universally required by law for everyone who drives to own and maintain. And in a country where the automobile has reigned supreme (at least up to a certain point), that’s a pretty big deal.

But I don’t have to tell you that auto insurance is huge business - you probably already knew that, or at least realized it without thinking about it. And before I spent some time working on the fringes of the insurtech industry, I knew that it was a big deal. But once I started really digging into it, did I realize just how big and, what’s more, how crazy competitive it is too.

There are massive incumbents who throw a lot of weight around in the space, trying to gain minor portions of market share. The industry does grow about 3-5% per year, but that’s not enough growth to feed incumbents and a whole bunch of newcomers. Barely gaining an inch is viewed as a great success in this semi-cutthroat industry. Okay: maybe cutthroat is too dramatic of an adjective, but it was far more competitive than I had imagined. And some do way better than gain an inch. But you get the point - it’s like any saturated, big market: competitive.

The Auto Insurance space was also much more technologically advanced than I was anticipating. My pre-conceived notion was that the industry was the ultimate incumbent-foil to tech’s disruptive upstarts - they were slow to move, and fat and happy. While there are some solid justifications to believe that narrative, I don’t think that’s a totally accurate representation. Most insurance carriers have strong internal technology teams, invest big dollars into their products, and have to move quickly in order to keep up with their competitors. And while some of them certainly have grown fat over the years, I was not under the impression that any were really that happy about the status quo. Growing their business is the name of the game and that’s how they get paid.

I am a big believer in incentives. Their incentives aren’t predicated on maintaining the status quo. However, the industry’s upper-bound is regulated into existence. As a result, many insurance co’s are focused on winning market share, not creating it. [Some, including the one I worked for, do a great job and think outside of the box, punching above their weight]. And that’s perfectly fine and reasonable - but it certainly rubs them the wrong way when newcomers enter the fray.

And in 2015, a newcomer entered the fray, in a fairly big way: Root Insurance. Over the course of the past five years, Root has experienced textbook rocket ship growth. This ludicrous-speed growth has made Root the belle of the ball in the Midwest tech scene, as well as the insurtech scene. When people talk about “Insurtech’s”, they are almost always having a conversation about Root, in one way or another. And for good reason - Root has been the most effective company to take on the incumbent insurance industry in years. And what’s more, they did it based in a college town like Columbus, Ohio.

However, Root, despite it’s obscene growth (which I will get to in a second), still only maintains a <1.0% market share of the auto insurance segment. Sure, even a tiny slice of a massive pie can feed a lot of people. However, there are some much bigger mouths to feed at the insurance carrier dinner table, so to speak. The Company, in it’s mission (whether stated or not) to upturn the auto insurance sector, is just getting started.

And while I mean that in a positive, optimistic manner, it should be noted that this also means that Root has a long way to go. They are, right now, a solid insurtech. But if they want to take over the insurance world, I think they still have room to run. I doubt anyone over there would deny that and I also don’t think it takes away anything that they have accomplished.

It is not surprising, however, that they picked 2020 to go public. They have experienced unbelievable growth over the past several years, raised silly amounts of capital, and built a great organization. And while some of their pure insurance stats are still sideways (or upside-down), one of the most important ones is on track for greatness - customer acquisition. Not only that, but 2020 has shown a particular penchant for tech stocks. And while you might argue that a company like Root isn’t a tech stock (for the time being, I would argue that it is), the market certainly doesn’t see it that way. And, luckily (or unfortunately, given a certain point-of-view), Root was able to witness dry run of how it’s IPO would go earlier this year when its renter’s insurance body-double Lemonade went public. Much to the joy of a lot of folks at Root, that IPO went pretty well. Unfortunately for Root, that stock hasn’t exactly stood the test of (incredibly short) time. Although, it still does have a $2.65 billion market cap - so not everything is all that bad.

So before Root went public, I am sure there were a lot of folks wringing their hands while they were watching that stock price. However, Root didn’t have much to worry about, because, on Wednesday, October 28th, Root’s offering went off without a hitch. While there was no customary first day tech stock “pop”, the company’s stock traded right above range, for a whopping current market cap of $6.4 billion.

So what went into that valuation? There are some very solid nuggets from the Company’s S-1 Filing.

S-1 Details

In the past, I have written about what makes a “tech company”. And while my conclusion continues to be: every company is moving toward becoming a tech company and that phrase is effectively meaningless, I do think there are some narrative tools that you can use to frame your company to make it sound more tech. Talk of disrupting industries, unseating incumbents, fundamentally rethinking the way things are done, etc. - these are all phrases you can find in a tech company’s language about itself. These are all things you can find in Root’s S-1. Why does that matter? Because in order for Root to achieve a valuation of a tech company, it has to convince investors it is more than just an insurance company (for the record, I think it is more than just an insurance company).

At the heart of Root’s tech story is their behavioral data and telematics. They are using data science and an app on your phone to write better rates. That’s what puts the tech in tech company here. That’s what puts butts in seats at Root’s IPO roadshow. They aren’t just selling insurance - they have found a way to take data and technology to sell better insurance. What’s important to note: almost all of the big and medium sized carriers are using telematics, in one way or another - either on a phone app, via an in-car dongle, an RFID sticker, or something along those lines. However, Root is probably the only one that is doing it on its entire book of business.

Importantly, Root’s competitive advantage is not the telematics, but it’s the scale at which they have deployed the telematics. As they continue to grow their book of business, their telematics data will, in theory, grow strong and more precise - better identifying driver risks, making them more profitable. This is a classic tech narrative - “our model will get better as it gets bigger because we will know more”. There are plenty of instances where that holds true… and plenty where it falls flat on its face.

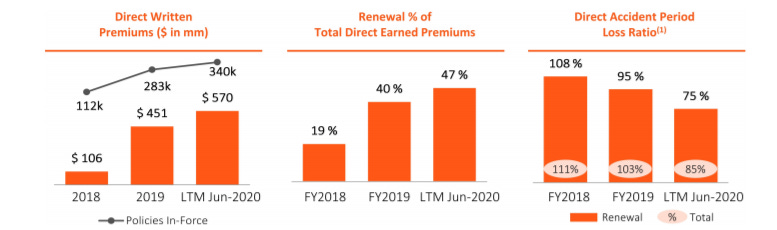

So it becomes imperative that the company grows rapidly. As of right now, they are burning through cash pretty quickly, but growing immensely to make up for it, hopefully making them more profitable from a unit perspective along the way. Below is a chart ripped from the S-1 that tells you a lot of what you need to know - the Company has quintupled (probably more) since 2018, and certain insurance-focused stats appear to be improving.

However, the Company still hasn’t been able to turn on the cash flow spigot just yet. It’s net losses have grown alongside it’s topline revenue, however, the hemorrhaging seems to be slowing down, relatively to how much money is coming in. The bleeding is still bad, but as a percentage of revenue, it has slowed down.

In insurance, there is an important ratio called the Combined Ratio that is effectively the gold standard for determining profitability of an insurance carrier. It is calculated by adding incurred losses and expenses, and then dividing that sum by earned premium. In other words, it provides a margin of how much money is flowing out in the underwriting process compared to how much is earned. A company with a combined ratio below 100% is doing well, making money. The cream-of-the-crop Combined Ratios in the industry float between 90 - 95%, while struggling insurers are above 100%.

This important ratio is nowhere to be found in Root’s S-1. This was not a clerical error - it’s a deliberate omission because, just based on back-of-the-napkin calculations, this ratio for Root is upside down. And while that could mean a death sentence for a publicly traded insurance carrier, it’s not as big of a deal for Root. [You might have a problem with that (I don’t blame you!), but you are better off being upset with Jerome Powell and other market conditions that have led to a wild bull market in the tech space].

This is the Company that is trying to radically alter the landscape of insurance - they aren’t going to do this by being conservative. They have to spend big if they want a bigger piece of the pie.

There is way more to unpack in this S-1, but the punchline is pretty straightforward: Root is growing like crazy, it’s wildly unprofitable (but getting better), and its strategy for world-domination is not that nuts. While I don’t use this blog to give investment advice (seriously, never take investment advice from this blog), the core thesis of buying this stock has to be: at $6 billion, Root is either hilariously overvalued or hilariously undervalued. Overvalued if you take a snapshot of a moment in time and compare them to every other auto insurance carrier. Undervalued if you buy their growth story, and assume they are going to take this business model to the moon.

What Does this Mean for Ohio

When Netscape went public in 1995, it marked a turning point for internet companies. It’s the inflection point that saw the internet fervor of the late ‘90’s really get going. (At least, that’s what my history books tell me - I was three years old in 1995). It paved a path for ways to liquidity that was previously little seen. And while Netscape wasn’t based in Silicon Valley, it made a big impact on Silicon Valley-type companies that would go on to define the back-half of the decade.

Root has potential to do that for Columbus, Ohio and maybe even all of Ohio. It’s not the first billion dollar exit in the region, but it’s by far the biggest. It will have the widest reach as far as creating a new class of angel investor in town, and it is going to radically alter the tech landscape for future years. I don’t know what the lockup provisions are for the employees who are executing their options right now, but I assume they are standard terms. So in a couple of short months, there are going to be a lot of folks who know what a successful tech company looks like, have made generational wealth on the backs of “investing” in tech, and are more likely to write angel checks. That’s a huge deal for a region like Ohio, which has Angel Investors, but not nearly enough.

What’s more: Root tells a very compelling story to VC’s that Ohio is a place to build great companies. Root’s biggest early backers (Drive Capital) are based in Central Ohio, but it was able to raise a lot of capital from folks not from around here. That’s a good thing - the more diversity we have in our funding ecosystem, the better. Root might have provided the roadmap for future VC’s flying into Cleveland, Cincinnati, or Columbus and writing big checks. The talent exists here. The infrastructure exists here. A lot of good investors already knew that - Root just made the story that much more compelling.

Friday Links

Inside the demise of one of Cincinnati's most-promising startups

Eccrine Systems - a super interesting startup based in Cincinnati, Ohio - recently announced that it was shutting down its business and pursuing a sale of company or assets. While this is a tough blow for the Cincinnati Startup Community, it’s an important reminder of two things: (1) starting a business, regardless of how well funded you are, is really hard and (2) we need to celebrate our failures like this and encourage these entrepreneurs and company employees to continue the pursuit. A failed startup is not something to scoff at - it’s an important, necessary part of any tech ecosystem. It shouldn’t be celebrated, but it should be venerated, so long as it didn’t fail on account of morally hazardous reasons.